One of the important discussion among mortgage holders is how do i pay off mortgage sooner, while the interest rate is one factor, the most powerful tool you have is actually your repayment strategy.

Making extra repayments even small amount is one of the most effective ways to reduce the total interest you pay and shave years off your mortgage.

The reason it works so well is due to compounding interest in reverse. Most home loans calculate interest daily based on your outstanding balance. When you make an extra payment, 100% of that money goes toward the “principal” (the actual amount you borrowed). By lowering the principal faster, you reduce the amount of interest the bank can charge you the following month, which creates a snowball effect.

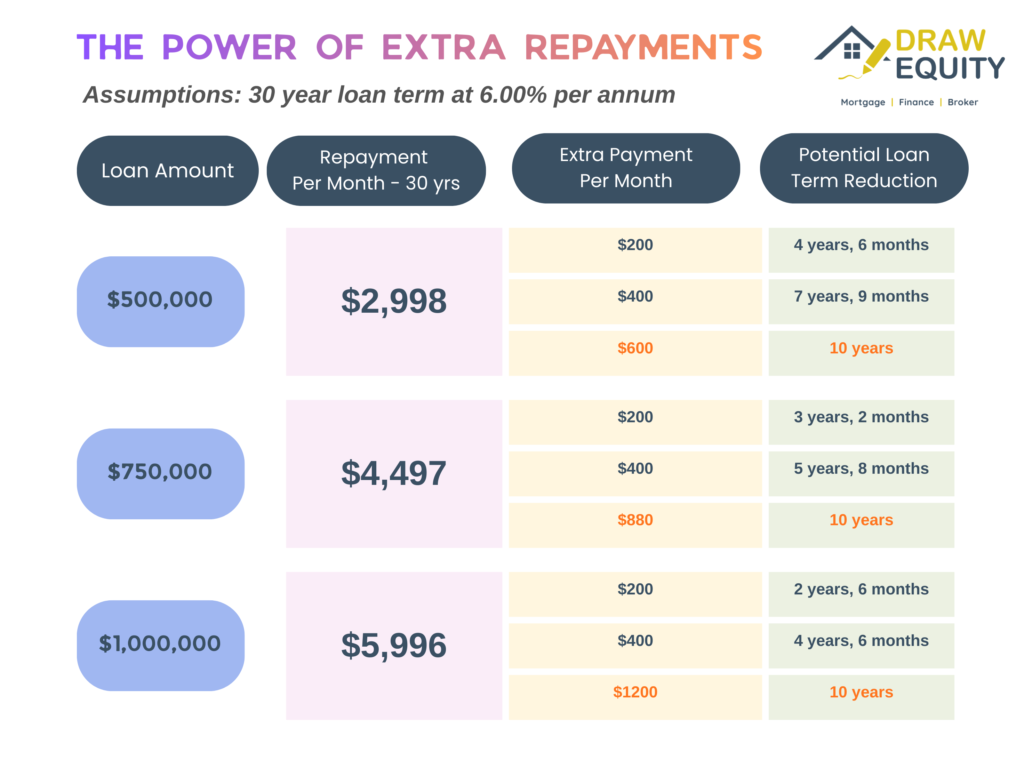

The Impact of Extra Repayments

The table above shows how much time you could save in various scenarios. The table includes two scenarios on each loan amount how long term you can reduce by paying $200 and $400 extra per month and it also includes 3rd scenario what repayment you need to pay to reduce loan term by 10 years in those loan amounts.

The Mindset of Successful Re-payers

People who successfully pay off their mortgages years ahead of schedule usually share a specific set of psychological traits. It’s rarely about having a massive salary; it’s almost always about discipline, perspective, and “game-planning” their debt.

Here are the four primary mindsets of the “Early Pay-Off” crowd:

1. The “Owner, Not Renter” Perspective

Many homeowners subconsciously feel like they “rent” from the bank for 30 years. Early payers shift this mindset to realize that until the debt is $0, the bank is a co-owner of their front door.

The Thought: “I don’t truly own my home yet; I’m buying my freedom back from the bank one square meter at a time.”

The Action: They view every extra $100 as purchasing a piece of their house forever.

2. The “Interest Hater” (The Math-Focused Mindset)

These people are driven by a healthy “dislike” for interest. They understand that on a standard 30-year loan at 6%, they could end up paying back double what they borrowed.

The Thought: “Every dollar of interest is money I’m giving away for nothing in return. I’d rather that money stay in my pocket than the bank’s.”

The Action: They look at their monthly statement specifically to see the “Interest Charged” figure drop. Their goal is to make that number smaller every single month.

3. The “Pay Yourself First” Discipline

Rather than seeing what is left over at the end of the month (which is usually $0), they treat their extra mortgage repayment like a mandatory bill.

The Thought: “My future self is my most important creditor.”

The Action: They set up an automatic transfer for $50, $100, or $200 to hit the mortgage the same day their salary hits their account. If they don’t see the money, they don’t miss it.

4. The “Gamification” Strategy

This mindset treats the mortgage like a video game or a challenge. They look for “wins” in their daily life to “attack” the balance.

The Thought: “I just saved $40 on this grocery shop—let’s see what that does to the loan balance.”

The Action: They use their banking app constantly. Did they get a $500 tax return? It goes to the loan. A $20 birthday gift? To the loan. They find psychological satisfaction in watching the principal balance drop below “milestone” numbers (e.g., getting it under $400k or $300k).

How to Make Extra Repayments Effectively

You don’t need to call the bank to do this. Most Australian lenders make it incredibly easy via their mobile apps:

-

- Set up a Recurring Transfer: Log in and set a scheduled “Pay Anyone” or “Internal Transfer” to your loan account to occur every payday or the cycle that suits you best.

-

- The “Manual Top-Up”: Whenever you have a “win”—like a tax return, a work bonus, or even a week where you spent less than usual—open the app and transfer that specific amount immediately.

If you like us to calculate the specific extra repayments for a different interest rate or a different loan term? Please click here to contact us and we can discuss those steps with you.