On Tuesday 12th of May 2026, Australian Treasurer Jim Chalmers handed down this years budget with some of the biggest changes to personal and investment taxes in decades.

Below are the key changes that will impact Property owners and buyers.

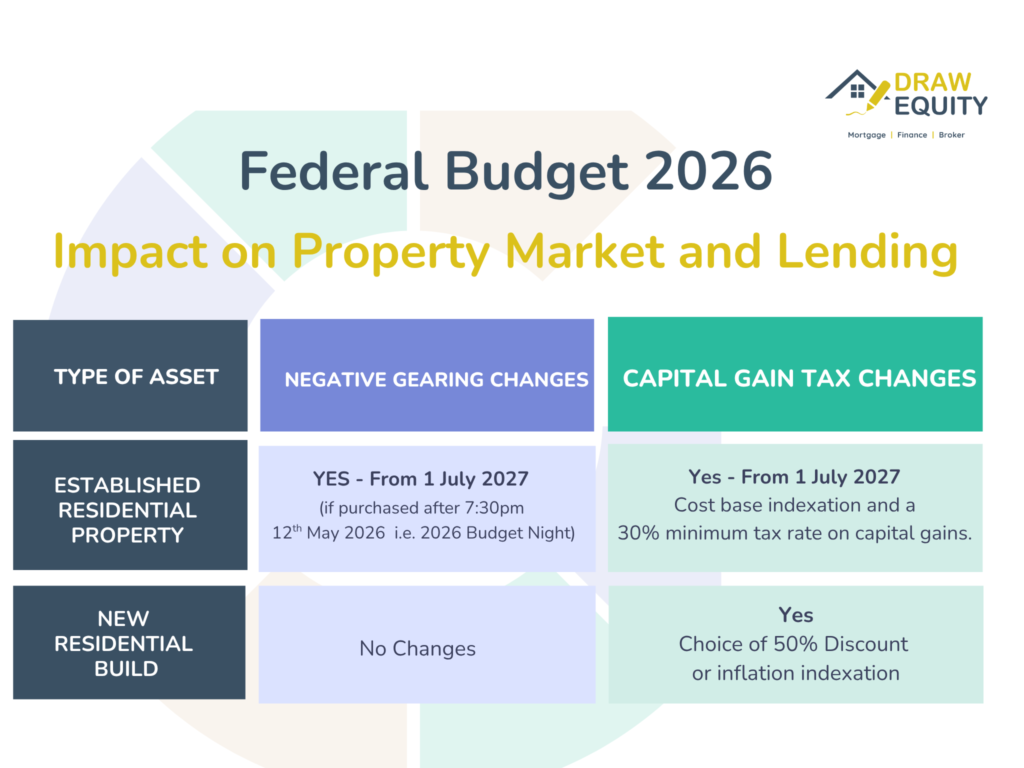

Investors – Negative Gearing

Negative gearing is a common financial strategy in Australia where the cost of owning an investment property (interest on the loan, maintenance, rates, and depreciation) is higher than the rental income it generates.

This results in a net rental loss, which can generally be used to reduce your taxable income from other sources, such as your wages.

From 1 July 2027, negative gearing for residential property will be limited to new builds only, removing the tax advantage for investors purchasing established homes. Properties already owned — or under contract — before 7:30pm AEST on 12 May 2026 (budget night) are fully exempt, so existing investors are not affected. Investors in affordable housing programs are also exempt.

What this means in practice:

Investors who buy established housing after budget night will still be able to deduct losses against residential property income and carry forward unused losses to future years, but will not be able to deduct them against other income like wages.

On these illustrative assumptions, the removal of negative gearing is equivalent to roughly a 90‑155 basis point increase in investor mortgage rates in immediate cash‑flow terms.

Existing investment properties will be grandfathered, so arrangements will not change for existing investors. This reduces the risk of forced sales, but it also creates a lock‑in effect by giving existing investors a stronger incentive to hold rather than sell.

Capital Gain Tax (CGT) discount

The second major change is to capital gains tax. From 1 July 2027, the existing 50% CGT discount for individuals, trusts and partnerships will be replaced with indexation and a 30% minimum tax rate. Investors will no longer receive a fixed 50% discount on nominal capital gains under the new arrangements. Instead, taxable gains will be calculated after adjusting for inflation, with real gains subject to the minimum tax rate where relevant.

This changes the after‑tax return profile of housing investment. Under the previous system, investors benefited from a large tax concession when nominal house price growth was strong. Under the new system, the tax outcome depends directly on the real capital gain.

Investors will still be protected from paying tax on the inflation component of the gain, but gains above inflation will be taxed at the investors marginal tax rate. Transitional arrangements mean the new rules apply only to gains arising after 1 July 2027.

The main residence CGT exemption and superannuation tax arrangements are not affected.

First‑home buyers

First home buyers may get a clearer run. The reforms should reduce investor competition in the established property market, which is the clearest affordability channel. However, the benefit is unlikely to fully match the fall in investor demand. Existing investors may hold rather than sell, reducing listings. Others may shift toward newly built dwellings, where negative gearing is retained. As a result, first‑home buyers should face less competition, but the affordability gains may be partly diluted by lower turnover and demand shifting elsewhere.

The Government said the changes to negative gearing and CGT discounts should help an extra 75,000 first home buyers enter the property market over the next decade.

Scenario – Impacts on existing property investors (From budget.gov.au)

Michael owns an investment property purchased before 12 May 2026 (budget night) that is negatively geared. He can continue to negatively gear this property in future years by using losses from his investment property against other income.

Michael sells the property two years after the policy commences for $560,000. Michael still receives the 50 per cent CGT discount for the capital gain he makes on the property between the purchase date and 1 July 2027.

He uses ATO tools to determine its value on that date was $500,000. After adjusting for two years of inflation of 2.5 per cent, his taxable capital gain for the period after 1 July 2027 is $34,688, slightly more than if he had applied a 50 per cent discount (which would have resulted in a taxable capital gain of $30,000). Assuming a 47 per cent tax rate, the tax on his gain since 1 July 2027 is $16,303 (instead of $14,100 with a 50 per cent discount).

Michael does not pay any tax on the capital gain until he sells his property.

How it impacts the Property market?

While the headlines focus on the immediate tax changes, the actual market shift will likely be a slow burn. Because the negative gearing changes are grandfathered and don’t fully take effect until July 2027, we expect a ‘transition phase’ where investors recalibrate their portfolios. This means the impact on property values and rental yields will emerge over years, not weeks, giving you a strategic window to review your holdings before the new landscape is fully set.

There may be lending rule changes coming up from lenders as currently negative gearing helps to increase borrowing power however in future that may not be possible for borrowers who wants to buy established property. We will share more information when we get updated from Banks and Lenders.

Please click on the link below to read more about the announcement related to CGT and negative gearing.